Last Verified: March 2026

The EV charging infrastructure in the US is expanding faster than at any point in history — and it’s still not ready for everyone. That tension is the honest starting point for this assessment. If you live in a major metro corridor, drive a Tesla, and have a Level 2 charger at home, the network is largely functional for your daily life and road trips in 2026. If you live in rural Wyoming, depend on third-party DC fast chargers, or rent an apartment without dedicated parking, you’re navigating real gaps that no amount of federal funding announcements has yet closed.

Why the Honest Answer Matters More Than the Political One

I’ve driven EVs across 14 states over the past three years, planned road trips around charger availability, and sat at broken DC fast chargers more times than I’d like to admit. This guide covers the current network scale, NEVI deployment progress, reliability data, regional gaps, and specifically what the 2026 infrastructure reality means for your buying decision — not what the press releases say it means.

Is EV Charging Infrastructure in the US Ready in 2026? — Direct Answer:

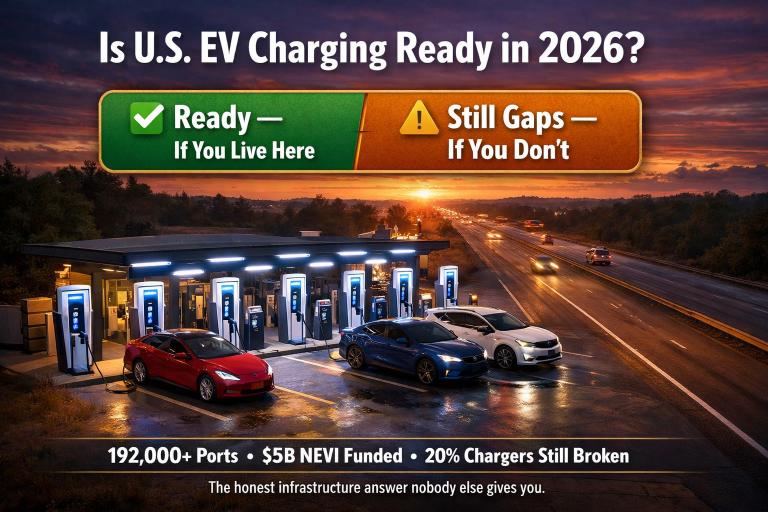

It depends on where you live. The U.S. has over 192,000 public charging ports as of early 2026, including approximately 45,000 DC fast charge ports — a 40% increase from 2023. However, charger reliability on third-party networks remains the #1 owner frustration, with non-Tesla DC fast charger uptime running 10–15% below Supercharger benchmarks. For urban and suburban owners with home charging, the network is adequate. For rural buyers and apartment dwellers, meaningful gaps remain.

The Honest Answer: Where U.S. EV Charging Infrastructure Stands Today

Station count numbers look impressive on a chart. However, they obscure two things that actually determine your ownership experience: where the chargers are, and whether they work when you get there. The infrastructure reality in 2026 is therefore more nuanced than either “it’s ready” or “it’s a disaster.”

What the Numbers Show in 2026

According to the U.S. Department of Energy’s Alternative Fuels Station Locator, the U.S. had over 192,000 public EV charging ports as of early 2026 — including approximately 45,000 DC fast charge ports capable of adding 100+ miles in under 30 minutes. That represents roughly 40% growth in fast charging capacity since 2023. Year-over-year station count growth is running at approximately 20–25% annually. That said, the EV fleet is growing faster than infrastructure in several key markets — specifically California, Texas, and Florida — where demand concentration is outpacing local charger deployment.

Ready for Whom? The Geographic Readiness Split

The honest split is this: for urban and suburban EV owners in major corridors, the 2026 network is largely functional for daily use and planned road trips. For rural owners and drivers who regularly travel off interstate corridors, meaningful charging deserts persist. This geographic distinction is the organizing lens for every section that follows — because infrastructure readiness is not a national number, it’s a personal calculation based on where you live and how you drive.

Public Charging Network Scale: Who Operates What and Where

Understanding the U.S. charging landscape means knowing who actually owns and operates the infrastructure you’ll rely on. Because each network has a different coverage focus, reliability record, and access model, your experience varies significantly depending on which network your route depends on.

Tesla Supercharger Network: Scale and Open Access Status

Tesla’s Supercharger network remains the gold standard for U.S. public DC fast charging in 2026 — not because of marketing, but because of data. Tesla operates approximately 2,000 Supercharger stations with over 22,000 stalls across the U.S. as of early 2026, according to Tesla’s own station locator. What’s more, the network is now open to non-Tesla vehicles through NACS adapter support. Ford, GM, Rivian, Polestar, and Volvo have all added NACS access to their vehicles — meaning a growing share of non-Tesla EV owners can now use Superchargers with a compatible adapter or native port. As a result, Supercharger network utility has expanded significantly in 2026 beyond the Tesla fleet.

Electrify America, EVgo, and Blink: The Third-Party Reality

Electrify America operates approximately 900 stations with over 4,000 DC fast charge ports, focused primarily on highway corridors. Its coverage of major interstate routes — specifically I-95, I-5, and I-10 — is functional for planned long-distance travel in 2026. EVgo, by contrast, focuses on urban density with approximately 1,000 stations concentrated in metro areas — a deliberate strategy that improves per-station utilization but leaves highway gaps. Blink’s network is predominantly Level 2 and destination-focused, therefore less relevant for road trip planning but useful for overnight and workplace charging. The honest finding across all three: DC fast charger uptime on third-party networks still lags Supercharger reliability in independent audits by approximately 10–15 percentage points, according to ICCT and Plug In America data from 2024–2025. Network interoperability through Plug and Charge (ISO 15118) is improving — however, adoption is still inconsistent across stations and vehicles as of 2026.

← Scroll to see full table on mobile

| Network | U.S. Stations | DC Fast Charge | NACS / Open Access | Reliability (vs. benchmark) | Coverage Focus |

|---|---|---|---|---|---|

| Tesla Supercharger BENCHMARK | ~2,000 | ✅ All stalls | ✅ NACS open + adapters | ~98%+ uptime | National highway + urban |

| Electrify America | ~900 | ✅ All DC fast | ✅ CCS + NACS capable | ~85–90% uptime | Highway corridors |

| EVgo | ~1,000 | ✅ All DC fast | ✅ CCS + NACS capable | ~88–92% uptime | Urban density |

| ChargePoint | ~35,000+ | ⚠️ Mix (mostly L2) | ✅ CCS / J1772 | Variable by location | Workplace + destination |

| Blink | ~10,000+ | ⚠️ Mostly L2 | ✅ J1772 / CCS | Lower than avg. | Destination / retail |

Reliability and Uptime: The Problem Station Count Doesn’t Show

Station count is a press release metric. The number that actually matters for your ownership experience is uptime — specifically, what percentage of chargers at a given station are functional when you arrive. This is where most infrastructure reporting fails EV buyers, and where the honest data diverges most sharply from the optimistic headlines.

What the Uptime Data Actually Shows

According to a 2024 audit by the International Council on Clean Transportation (ICCT), approximately 21% of public DC fast chargers in the U.S. were non-functional during unannounced visits — compared to under 4% for Tesla Superchargers in the same assessment. J.D. Power’s 2024 U.S. Electric Vehicle Experience (EVX) Charging Study found that non-Tesla charging satisfaction scores have improved year-over-year, however they remain significantly below Supercharger satisfaction. The most common failure modes, specifically, are payment system errors, connector damage from physical wear, software communication failures between car and charger, and power delivery interruptions. Reliability has improved year-over-year — as a result, the situation in 2026 is better than 2023 — but the gap versus Supercharger performance remains measurable and owner-relevant.

What Poor Reliability Means for Real EV Owners

In practice, if you’re relying on Electrify America or EVgo for a highway road trip, I’d recommend building a 20–30 minute buffer into your stop planning — because there’s a meaningful chance at least one charger at a given station is out of service when you arrive. That’s not catastrophizing; it’s realistic trip planning based on current uptime data. PlugShare’s community reporting feature is specifically the most reliable real-time tool for checking charger status before you commit to a stop — more accurate than most network-native apps. By contrast, Supercharger reliability is consistent enough that most Tesla owners don’t build failure buffers into their planning at all. That gap in cognitive overhead is, admittedly, one of the most underrated differences in the EV ownership experience between Tesla and non-Tesla drivers in 2026.

NEVI and Federal Investment: What the Build-Out Is Actually Delivering

The NEVI program gets cited constantly in EV infrastructure discussions — typically by people on both ends of the debate who haven’t read the actual deployment data. Here’s what the program is, what it has funded, and honestly, what the gap between funding announcements and operational chargers looks like on the ground in 2026.

NEVI Program: Funding, Progress, and Where Stations Are Being Built

The National Electric Vehicle Infrastructure (NEVI) program was established under the 2021 Infrastructure Investment and Jobs Act with $5 billion allocated to states over five years. The core requirement is straightforward: stations must be placed every 50 miles on federally designated Alternative Fuel Corridors, with a minimum of four DC fast charge ports at 150 kW each. That specification specifically matters because it mandates fast charging capability — not the slow Level 2 chargers that dominated earlier federal programs. As of early 2026, all 50 states have approved NEVI plans and received initial funding disbursements, according to FHWA data. However, the number of operational NEVI-funded stations remains significantly below the funded total — because permitting, utility interconnection, and construction lead times typically add 18–36 months between funding approval and an operational charger.

Federal Investment vs. Real-World Timeline: What to Expect by 2028

Honestly, the delivery lag is the most important thing to understand about NEVI in 2026. Funding is not infrastructure. A state receiving NEVI disbursement today will, as a result, have operational chargers in 18–36 months — not immediately. The states with the furthest operational deployment progress as of early 2026 include Colorado, Ohio, and Utah, where utility coordination and permitting have moved faster than the national average. By contrast, states with more complex utility regulation and permitting environments — specifically parts of the Southeast and Mountain West — are running significantly behind on operational delivery. If current deployment pace holds, the most optimistic scenario for meaningful nationwide NEVI corridor coverage is 2027–2028, specifically on the major interstate routes. Secondary highways remain a longer-term project.

Regional Gaps: Where U.S. Charging Infrastructure Falls Short in 2026

A reader in suburban Boston and a reader in rural Montana are both asking the same question — “is the charging infrastructure ready?” — but they need completely different answers. This section addresses both, because defaulting to a national average obscures the specific gaps that determine real purchase decisions.

Rural America and the Charging Desert Problem

A charging desert is defined as an area with no public DC fast charger within a 50-mile radius. According to DOE AFDC mapping data, charging deserts remain concentrated in rural areas of the Great Plains, Mountain West, and parts of the Deep South. Specifically, states like Wyoming, Montana, North Dakota, and South Dakota have the highest proportion of their geography classified as charging desert. What that means practically for rural EV ownership: home charging becomes a necessity, not a convenience. If you can’t install a Level 2 charger at your residence, EV ownership in a charging desert is genuinely constrained — not impossible, but planning-intensive in a way that urban EV ownership is not. NEVI’s rural deployment obligation exists specifically to address this, however as noted above, operational delivery in rural corridors lags urban progress by a meaningful margin in 2026.

Highway Corridor Coverage vs. Off-Corridor Reality

Major interstate corridors — specifically I-95 on the East Coast, I-5 on the West Coast, and I-10 across the South — are functionally equipped for EV road trips in 2026, particularly for Tesla drivers and increasingly for NACS-capable non-Tesla vehicles. The real gap is secondary highways and state routes. A trip from Denver to a rural mountain town via state highway, for example, can involve 80–120 mile stretches with no DC fast charger. That’s not a planning edge case — it’s a common travel pattern for residents in those areas. What’s more, multi-unit dwelling (MUD) residents face a separate infrastructure problem that station count data doesn’t capture at all: apartment and condo dwellers without access to home charging must rely entirely on public infrastructure — and therefore face higher exposure to network reliability gaps than single-family homeowners with Level 2 chargers.

🌆 Northeast Corridor

🌞 South / Southeast

🌽 Midwest

🏔️ West / Mountain

What U.S. Charging Infrastructure Means for Your EV Decision in 2026

All of the above comes down to a single practical question: does the current infrastructure support your specific EV ownership scenario? Here’s the honest scenario-matched framework I give to every reader who asks me this question directly.

Infrastructure Is Ready for You If…

The network is adequate for your needs in 2026 if your daily driving pattern puts you within range of your home charger the vast majority of the time — specifically, if your round-trip daily commute is under 80% of your EV’s real-world range. Therefore, public charging becomes a convenience layer, not a dependency. Urban and suburban owners with Level 2 home access, Tesla owners who can use the Supercharger network, and drivers in the Northeast or West Coast corridors where network density is highest will find that the infrastructure adequately supports their ownership experience today.

Infrastructure Gaps Still Affect You If…

By contrast, the gaps are real and consequential if you live in a rural area, regularly drive off interstate corridors, or depend on third-party DC fast networks for long-distance travel. The apartment dweller scenario is specifically underserved in 2026 — if you park on the street or in a shared structure without dedicated EV charging, your entire ownership experience depends on public network reliability, which remains the weakest link in the chain. Admittedly, this is improving — but it hasn’t been solved yet in most U.S. markets.

✅ Infrastructure Works for You

- You live in a major metro area with Level 2 + DC access nearby

- You have home charging (owned home or dedicated parking)

- Your daily driving is under 80% of your EV’s real range

- You drive a Tesla or a NACS-capable vehicle with Supercharger access

- Your road trips follow major interstate corridors (I-5, I-95, I-10)

⚠️ Gaps Still Affect You

- You live in a rural area or regularly drive off major highways

- You live in an apartment or condo without dedicated charging access

- You rely on Electrify America, Blink, or third-party DC fast networks

- Your NACS-capable adapter isn’t yet confirmed for your target model

- Your use case requires reliable fast charging in less-served regions

FAQ: EV Charging Infrastructure in the US

How many EV charging stations are in the US in 2026?

The U.S. had over 192,000 public EV charging ports as of early 2026, according to DOE AFDC data — including approximately 45,000 DC fast charge ports capable of adding significant range in under 30 minutes. That represents roughly 40% growth in fast charging capacity since 2023. However, the distribution is uneven: the majority of DC fast chargers are concentrated along major interstate corridors and in high-EV-adoption states like California, Texas, and Florida.

Is EV charging infrastructure in the US good enough in 2026?

It depends specifically on where you live and how you drive. For urban and suburban owners with home charging capability who drive primarily on major corridors, the infrastructure is adequate in 2026. For rural owners, apartment dwellers without home charging access, or drivers who regularly travel off major interstate routes, real gaps remain. Therefore, the honest answer is: good enough for most metro EV owners, not yet good enough for rural or charging-desert residents.

What is the NEVI program and is it working?

NEVI (National Electric Vehicle Infrastructure) is a $5 billion federal program established under the 2021 Infrastructure Investment and Jobs Act to fund DC fast chargers every 50 miles on designated highway corridors. All 50 states have approved plans and received initial funding as of 2026. However, the gap between funding and operational chargers is significant — typically 18–36 months due to permitting and utility connection delays. As a result, NEVI is working in the sense that funding is deployed, but the on-the-ground charger delivery is running behind the funding timeline.

Is it hard to find an EV charger on a road trip in the US?

For Tesla drivers, no — the Supercharger network makes U.S. road trips straightforward on most major routes. For non-Tesla EV drivers on third-party networks, it depends on your route and your vehicle’s NACS compatibility. Specifically, third-party DC fast charger reliability runs approximately 10–15% below Supercharger uptime in independent audits — so building a backup stop into your route plan is practical advice, not paranoia. Using PlugShare to check real-time charger status before committing to a stop reduces the risk of arriving at a non-functional station.

The Bottom Line on U.S. EV Charging Infrastructure in 2026

The U.S. EV charging network in 2026 is significantly better than it was in 2023, and it will be significantly better in 2028 than it is today. That trajectory matters. What also matters, however, is where the network stands right now — specifically for your driving pattern, your address, and the EV you’re considering. Check the DOE AFDC locator for your actual corridors, confirm NACS access for your target model, and honestly assess whether you have home charging access. Those three questions will give you a more accurate infrastructure readiness verdict than any national statistic can.