Last Verified: March 2026

Five years ago, European buyers barely knew BYD existed. Today, BYD outsells Tesla in Europe — a milestone confirmed by Reuters in May 2025. That sentence alone tells you everything you need to know about why Chinese EVs are taking over Europe. This isn’t a gradual trend. It’s an industrial tipping point that caught legacy automakers flat-footed and is now forcing a complete rethink of how the European car market works.

Why 2026 Is the Year Europe Can No Longer Ignore This

The shift isn’t happening because of one factor — it’s happening because of seven overlapping ones. Price, battery technology, production speed, export strategy, consumer sentiment, legacy brand weakness, and charging infrastructure have all converged at the same moment. Specifically, as Europe’s cost-of-living pressure intensified, Chinese brands arrived with long-range EVs priced under €30,000 and tech features that match or beat vehicles costing €15,000 more. That’s not just competition. That’s a structural disruption. I’ve followed this market for over a decade, and what’s happening now is unlike anything I’ve tracked before.

Why Are Chinese EVs Taking Over Europe?

Chinese EVs are dominating Europe because they combine lower production costs, vertical battery supply chains, and faster software development into vehicles that undercut European prices by €10,000–€20,000 while matching or exceeding range and tech specs. BYD outsold Tesla in Europe for the first time in 2025. By 2027, Chinese brands are projected to hold 15–25% of Europe’s total EV market — rising to 30–35% in key countries by 2030.

The 7 Core Reasons Chinese EVs Are Dominating Europe

The rise of Chinese EVs in Europe isn’t luck. It isn’t a subsidized dumping operation. It is the outcome of structural advantages built over a decade — in batteries, software, supply chains, and execution speed — that European automakers simply cannot replicate quickly. Europe, meanwhile, is still transitioning from ICE infrastructure. The result is a widening gap that shows up in every metric: price, range, charging speed, and buyer satisfaction.

Here’s what’s actually driving this takeover — broken down by force, not by headline.

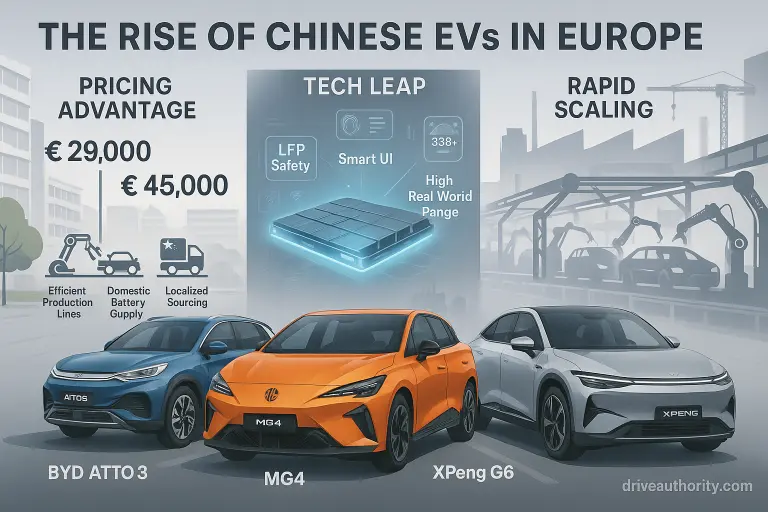

Pricing Advantage — High Tech at Lower Cost

If you ask a European buyer why they chose a BYD Atto 3 or MG4 over a local alternative, the answer usually starts with price. However, price alone isn’t the full story. What Chinese EVs offer is more technology for less money — and that equation is increasingly hard to walk away from.

Why Chinese EVs Cost So Much Less to Build

China produces more lithium batteries than the rest of the world combined. As a result, domestic automakers avoid the expensive battery imports that burden European brands. The entire supply chain — mining, cell production, pack assembly, and vehicle integration — operates as one optimized ecosystem. That end-to-end control eliminates the margin-stacking that happens when European OEMs buy from layered international suppliers.

When a buyer compares a European EV at €45,000 to a Chinese alternative at €29,000 offering similar range, infotainment quality, and safety ratings, the value speaks for itself. For households under cost-of-living pressure, this isn’t brand preference. It’s financial logic. Specifically, that €16,000 gap covers three years of fuel costs for most drivers — making the switch feel not just smart, but necessary.

Massive Tech Leap — Batteries, Software, and Range

This is the part of the story that surprises most people who haven’t driven a recent Chinese EV. The assumption is that lower price means lower quality. That assumption is wrong — and it’s getting more wrong with every model cycle.

LFP vs NMC: Why Battery Chemistry Matters

While many European automakers still rely heavily on NMC battery chemistry, Chinese brands have aggressively pushed LFP (lithium iron phosphate) technology forward. LFP batteries are more durable, thermally safer, cheaper to produce, and increasingly effective in cold-weather conditions. BYD’s Blade Battery — the most refined LFP implementation currently available — specifically addresses the cell-to-pack density problem that made earlier LFP batteries less attractive for long-range applications. As a result, BYD’s Seal and Dolphin now deliver real-world range that matches or beats NMC-based European competitors.

Honestly, I was skeptical about LFP range performance in European winters. Then I reviewed independent cold-weather tests showing the BYD Seal retaining over 80% of advertised range at -10°C — a result that challenged everything I assumed about that chemistry. Chinese EV tech is no longer catching up. In several categories, it’s already ahead.

Software, ADAS, and Infotainment That Feel Native

Beyond batteries, Chinese EVs have built infotainment and ADAS systems that feel genuinely smartphone-native — not automotive-native. That distinction matters enormously to younger buyers. By contrast, Volkswagen’s recurring software delays on the ID family remain the most visible example of how legacy automakers struggle with digital architecture. Chinese brands don’t carry that legacy burden. Therefore, their software development cycles are faster, their OTA updates are more frequent, and their in-car UX is more intuitive out of the box.

Production Speed and Scaling Power

One of China’s greatest competitive advantages isn’t a product — it’s a process. European automakers may spend four to six years developing a new EV platform. Chinese brands routinely design, validate, and launch a new model in 18–24 months. That speed difference isn’t incremental. It’s structural.

Vertical Integration Is the Engine

Most major Chinese EV manufacturers control every stage of production: batteries, motors, chips, operating systems, and raw material sourcing. BYD is the clearest example — it produces its own semiconductors, its own battery cells, and assembles complete vehicles under one corporate umbrella. As a result, when a component needs changing, the decision takes weeks rather than the multi-supplier negotiation cycles that slow European OEMs. Model updates roll out the way software updates do — not as generational redesigns that require years of platform investment.

BYD, CATL, and Geely collectively operate gigafactories across Asia and Europe. Capacity scales rapidly as global demand rises. That scalability means Chinese brands can respond to market signals — a new competitor, a price war, a regulatory shift — faster than any European equivalent. Speed isn’t just an advantage in this industry. It’s a form of market domination in itself.

Aggressive Export Strategy and Brand Positioning

China didn’t enter Europe by accident. The strategy was deliberate, state-supported, and calibrated specifically for the European consumer mindset. Each major Chinese brand targets a different buyer segment — and together they cover the entire market from budget to premium.

How Each Brand Owns Its Segment

| Brand | Segment | Core Advantage in Europe | Key Model |

|---|---|---|---|

| MG (SAIC) MASS MARKET | Affordable mainstream | Sub-€30K pricing, familiar heritage name, strong dealer network | MG4, ZS EV |

| BYD BEST VALUE | Mid-range value + range | Blade battery, vertical integration, best price-to-range ratio | Dolphin, Seal, Atto 3 |

| Xpeng | Tech-forward mid-range | ADAS, autonomous features, smart software ecosystem | G6, P7 |

| NIO | Premium / luxury | Battery swap in 5 minutes, lifestyle ecosystem, subscriptions | ET5, ET7, EL7 |

| Zeekr (Geely) | Design-led premium | Scandinavian-influenced design, premium interiors, OTA architecture | Zeekr 001, 007 |

This is not random expansion. It is coordinated market capture — each brand occupying a specific lane, minimizing internal competition while maximizing collective market share. By contrast, European OEMs are largely competing against each other in premium segments while the volume market shifts beneath them.

State-backed incentives for Chinese EV exporters also play a role. Specifically, localization deals — building locally in Hungary, Germany, and other EU countries — are actively reducing the tariff exposure that Brussels has tried to use as a barrier. As a result, the political protection that European automakers hoped for is increasingly being negotiated away.

Consumer Demand and Shifting European Perception

Five years ago, many European drivers viewed Chinese electric cars with genuine skepticism. Reliability, safety, and service support were open questions. Today, that skepticism is fading — and not because of marketing. It’s fading because of direct experience.

Trust Is Rising Because Performance Demands It

High Euro NCAP safety scores, strong real-world range consistency, and refined cabin quality have collectively dismantled old stereotypes. By 2024–2025, the question buyers ask has shifted. Instead of “Is it reliable?”, they’re asking “How does its range compare to the VW ID.4?” That’s a fundamentally different — and far more commercially dangerous — conversation for European brands. As a result, consumers are now benchmarking Chinese EVs against European models on their merits, not dismissing them on origin.

Why Younger European Buyers Are Leading the Shift

Millennial and Gen Z buyers are less tied to legacy brand identity and more focused on technology, price, and UX quality. They want smart connectivity, fast software, and stylish design at accessible price points. For many first-time EV owners, an MG4 or BYD Dolphin isn’t a compromise — it’s a rational first choice. Specifically, these buyers prioritize value-per-euro over brand heritage, and subscription-based ownership models, leasing programs, and fast OTA updates feel natural to them in a way they simply don’t for older demographics.

Fleet operators have accelerated the shift even faster than individual buyers. When a leasing company or corporate mobility program can reduce total cost of ownership by 20–30% by switching to Chinese EVs, the decision becomes economic, not emotional. That fleet-level adoption is creating visible, normalized presence on European roads — which in turn reduces hesitation among individual buyers.

Europe’s Legacy Automakers Are Falling Behind

The other half of this story isn’t just about Chinese strength — it’s about European weakness. Legacy automakers are struggling to adapt, and their decades of manufacturing excellence are now, in certain respects, working against them.

The Structural Disadvantages Europe Can’t Quickly Fix

European OEMs carry legacy ICE infrastructure, high labor costs, long development cycles, and layered multi-supplier relationships that slow every decision. When a Chinese brand needs to update its battery management system, it can push an OTA update in weeks. When a European OEM needs to do the same, it often requires supplier negotiations, validation cycles, and regulatory approval processes that span months. Volkswagen’s recurring software delays on the ID range are the most visible and most documented example of this problem — specifically, a challenge rooted in the fact that software was added on top of an automotive architecture rather than built into it from the beginning.

Europe isn’t just being outpriced. It’s being outpaced in the dimension that matters most in a software-defined vehicle era: iteration speed. As a result, younger buyers who evaluate cars the way they evaluate smartphones — by how smart, connected, and frequently updated they are — are finding Chinese EVs far more aligned with their expectations. That’s a brand perception problem that price cuts alone cannot solve.

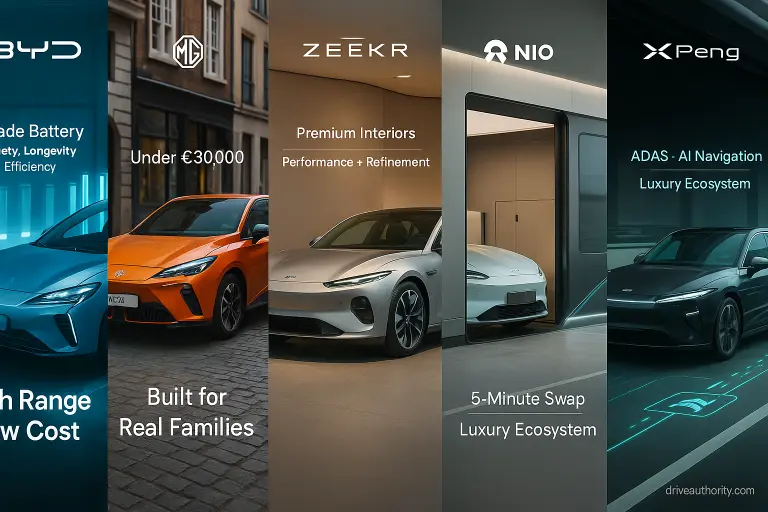

Brand-by-Brand: BYD, MG, NIO, Xpeng, and Zeekr

Not all Chinese EVs are equal. Each brand has a distinct strategy, a specific buyer target, and a different reason to be considered. Understanding those differences is how you make the right purchase decision — or the right investment thesis, if you’re watching this market from the industry side.

BYD — The Battery King

If one brand defines the rise of Chinese EVs, it’s BYD. Once a battery manufacturer, now a fully vertically integrated automaker with control over production, chemistry, semiconductor supply, and vehicle assembly. BYD’s Blade Battery technology is genuinely differentiated — it’s safer under thermal stress, more energy-dense per pack volume than competing LFP designs, and demonstrably more durable across high-cycle use. As a result, BYD vehicles — specifically the Dolphin, Atto 3, and Seal — deliver range and reliability benchmarks that undercut European competitors while costing less to buy. BYD outselling Tesla in Europe for the first time in 2025 wasn’t a fluke. It was years of structural advantage made visible.

MG (SAIC) — The Normalizer

MG plays a different game from BYD. Instead of leading on battery innovation, it leads on accessibility. The MG4 — priced under €27,000 in key European markets — has become the most successful Chinese EV for everyday buyers. The heritage British brand name reduces psychological friction for conservative buyers. The dealer network is the most developed of any Chinese EV brand in Europe. What’s more, leasing penetration is strong enough that MG is now a fixture in fleet and corporate mobility programs across the UK, Germany, and France. That visibility on European roads is itself a form of marketing that no advertising budget can replicate.

NIO — The Luxury Ecosystem

NIO approaches Europe with a strategy that no other brand — Chinese or European — has fully executed: battery-as-a-service. The ability to swap a depleted battery for a full one in approximately five minutes eliminates the single biggest friction point for long-distance EV users. That’s not a marketing claim. It’s an infrastructure investment NIO has made in its swap station network across key European cities. Combined with a premium sedan and SUV lineup (ET5, ET7, EL7) and a subscription-based ownership model, NIO is positioning itself as a luxury electric ecosystem — not just a car brand. By contrast, premium European EVs still require 20–45 minutes at a fast charger for an equivalent range top-up.

Xpeng — The Software Leader

If BYD owns batteries and MG owns mass-market penetration, Xpeng owns software. The brand is laser-focused on autonomous driving, AI-assisted navigation, and intelligent cockpit experiences that feel genuinely closer to a Tesla than to traditional European UIs. Specifically, Xpeng’s ADAS suite and highway navigation assistance are technically competitive with Tesla’s FSD in European regulatory contexts. Models like the G6 and P7 are built with aerodynamics, efficiency, and autonomy as primary design parameters. As a result, Xpeng appeals most strongly to younger, tech-oriented buyers who evaluate cars as connected devices rather than traditional machines.

Zeekr (Geely) — The Premium Challenger

Geely’s Zeekr brand is the most interesting long-term play in the Chinese EV portfolio. Rather than competing purely on price, it competes on design and material refinement. Zeekr interiors genuinely challenge Audi and BMW at comparable price points — the Scandinavian-influenced aesthetic reflects Geely’s ownership of Volvo and its deep familiarity with premium European design language. Therefore, Zeekr is positioned to capture buyers who want Chinese value-engineering without wanting to feel like they made a budget compromise. That’s a meaningful segment — and one European luxury brands are underestimating.

Challenges Chinese EVs Still Face in Europe

The takeover narrative is real — but it’s not complete. Chinese EVs face structural obstacles in Europe that will determine whether they achieve sustained dominance or plateau at a ceiling of politically and logistically constrained market share.

Tariffs, Trade Politics, and the Brussels Factor

The European Commission’s anti-subsidy investigation into Chinese EVs resulted in additional import duties of up to 35.3% on top of the existing 10% tariff — specifically targeting BYD, SAIC, and Geely in 2024. That’s a significant cost headwind. However, Chinese manufacturers are adapting by investing in local European production. BYD’s Hungarian factory and SAIC’s expansion in the UK are designed specifically to manufacture inside the tariff wall, thereby preserving the price advantage that drives adoption. That said, the political pressure isn’t disappearing — and any escalation in EU-China trade tensions could reshape the economics of Chinese EV imports rapidly.

After-Sales Infrastructure Is Uneven

Strong product isn’t enough for European buyers. Service support, spare parts availability, and repair infrastructure matter deeply — particularly for buyers outside major urban centres. Many Chinese EV brands have strong showroom presence in London, Paris, and Berlin, but rural coverage is thin. Certified service centre expansion is ongoing but uneven across countries. As a result, buyers in less-served regions face real ownership risk that urban comparison tests don’t reflect. This is specifically the challenge that MG has handled best — leveraging its existing dealer network to provide the closest thing to a complete ownership ecosystem among Chinese brands in Europe.

Long-Term Reliability Data Is Still Developing

Chinese EVs haven’t existed in Europe long enough to accumulate the 8–12 year reliability records that Volkswagen and Toyota can point to. Battery longevity looks promising based on current data, however consumers want evidence, not projections. What happens to these vehicles at 200,000 km? Will software support remain active for a car bought in 2023? How will second-hand values perform as the market matures? These are open questions. Admittedly, European brands face EV reliability uncertainty too — but they have decades of combustion-era trust to fall back on. Chinese brands are building that trust in real time, in the most demanding automotive market in the world.

What This Means for Europe’s Automotive Industry

The rapid growth of Chinese EVs in Europe is more than a market share story. It forces a strategic rethink across every layer of the industry — OEMs, suppliers, regulators, and investors. Below is the clearest breakdown I can offer of what’s actually changing and what the tradeoffs look like for each stakeholder.

What Legacy OEMs Must Now Decide

🏭 Path A — Compete on Volume

- Cut prices and accept lower margins to retain mass-market share

- Accelerate modular EV platforms to shorten development cycles

- Invest heavily in local battery production and vertical integration

- Risk: brand dilution, capital intensity, slower profitability recovery

- Best for: VW Group, Stellantis — brands with volume manufacturing scale

- Timeline: 5–8 years minimum to achieve structural cost parity

🎯 Path B — Defend Premium Segments

- Cede mass-market volume and focus on luxury, performance, and safety

- Leverage European design excellence and regulatory credibility

- Form targeted alliances with Chinese battery and software providers

- Risk: market footprint shrinks; long-term R&D leadership erodes

- Best for: BMW, Mercedes, Porsche — brands with genuine premium equity

- Timeline: immediately executable — but requires accepting market share loss

Pricing Reset and Supply Chain Realignment

Chinese EVs have already reset European pricing expectations. The €30,000 long-range EV is no longer aspirational — it’s the new baseline for what mainstream buyers consider fair value. As a result, European OEMs face mounting pressure to reduce list prices or deliver meaningfully more at current ones. Suppliers will be squeezed simultaneously — forced to cut costs or innovate toward higher-value integrated components to justify their position in the supply chain. What’s more, battery production concentration in Asia means Europe faces a binary choice: invest €40–60 billion in local gigafactory capacity over the next decade, or accept structural dependency on Asian battery supply for the foreseeable future. That dependency has geopolitical implications well beyond the automotive sector.

Future Outlook: Chinese EVs in Europe 2026–2030

The next five years will determine whether Chinese EVs remain aggressive challengers or permanently reshape Europe’s automotive hierarchy. Based on current trajectories confirmed by PwC Strategy& and independent market analysis, the direction is clear — even if the exact magnitude isn’t.

Market Share Projections by Year

| Period | Projected Chinese EV Share (Europe) | Key Driver | Risk Factor |

|---|---|---|---|

| 2025–2027 | 15–25% of total EV sales | Pricing, range, and tech advantages in compact/mid-range segments | EU tariff escalation |

| 2028–2030 | 30–35% in Germany, Norway, Netherlands | Maturing dealer networks, brand recognition, fleet normalization | European OEM response at scale |

| Post-2030 | Segment-dependent leadership | Chinese brands define mainstream pricing and feature expectations | Local production mandates |

Predictions for Top EV Brands in Europe by 2030

Based on current trajectories, market positioning, and brand strategy — here’s where I see each major Chinese brand landing by 2030:

| Rank | Brand | 2030 Position | Outlook |

|---|---|---|---|

| 1 | BYD LEADER | Mass-market volume leader among Chinese EVs | Battery advantage compounds; likely top-3 overall European EV brand |

| 2 | MG (SAIC) | Dominant in affordability segments | Broadest dealer footprint; normalized household brand in UK and Germany |

| 3 | Xpeng | Tech-driven adoption | Autonomous features attract digitally native buyers; software edge widens |

| 4 | NIO | Premium EV ecosystem niche | Battery swap infrastructure is a durable differentiator if rollout scales |

| 5 | Zeekr (Geely) WATCH | Boutique premium challenger | Strong design credentials; success depends on brand-building investment in EU |

Europe’s legacy brands will retain genuine strength in premium and performance EVs. However, mainstream segments — the volume that actually funds R&D and sustains large manufacturing footprints — may permanently tilt toward Chinese offerings unless structural investments in battery production, software platforms, and modular architectures are made within this decade.

FAQ: Chinese EVs in Europe

Are Chinese EVs reliable for European roads in 2026?

Based on current Euro NCAP results and real-world ownership data, yes — the major brands perform well. BYD, MG, and Xpeng have all scored 5-star Euro NCAP ratings on recent models, and ownership satisfaction among early European adopters is generally high. However, long-term data — specifically battery performance past 200,000 km and software support timelines beyond 8–10 years — is still developing. As a result, buyers should research specific model warranty terms and service network coverage in their region before committing.

Why are Chinese EVs so much cheaper than European ones?

The price gap comes from vertical integration. Because China produces more lithium batteries than the rest of the world combined, Chinese automakers avoid the import costs that burden European brands. They also control manufacturing, software, and component supply under one ecosystem — eliminating the margin-stacking that happens when European OEMs buy from multiple international suppliers. Specifically, the average price gap between a comparable Chinese and European EV in 2026 is approximately €10,000–€16,000 in the same segment, according to European showroom pricing analysis.

Which Chinese EV brand is best for European buyers in 2026?

That depends on your priority. For best overall value and range, BYD (specifically the Dolphin or Seal) is the strongest all-around choice. For the lowest upfront cost and broadest service coverage, MG4 is the practical winner — its dealer network is the most developed of any Chinese EV brand in Europe. For technology-first buyers focused on ADAS and software, Xpeng G6 is the standout. For premium buyers who want Chinese engineering with luxury-level interior quality, Zeekr 001 is worth serious consideration.

Do EU tariffs change the price advantage of Chinese EVs?

The EU’s 2024 anti-subsidy duties added up to 35.3% on top of the existing 10% tariff for major Chinese EV manufacturers. That’s meaningful — however it hasn’t eliminated the price advantage. BYD, SAIC, and Geely are actively investing in European local production specifically to manufacture inside the tariff wall. BYD’s Hungarian factory and SAIC’s UK operations are both designed to preserve competitive pricing despite import duties. That said, any further escalation in EU-China trade tensions could materially change the economics, and buyers should factor that political risk into long-term ownership planning.

How will Chinese EVs affect European car prices long-term?

They are already compressing prices. The €30,000 long-range EV has become the new mainstream benchmark — down from approximately €38,000–€42,000 just three years ago. By contrast, European OEMs face margin pressure as they try to match Chinese value propositions without the same structural cost advantages. PwC Strategy& projects that the average EV transaction price in Europe will fall significantly through 2030 as Chinese market share expands, benefiting buyers substantially while challenging OEM profitability. Fleet and leasing buyers are already seeing 20–30% total cost of ownership reductions by switching to Chinese EVs.

The Bottom Line on Chinese EVs in Europe

Chinese EVs are taking over Europe because they deserve to — not because of political manipulation, not because of dumping, and not because European buyers are settling. They’re winning because BYD, MG, Xpeng, NIO, and Zeekr built better products for the price, delivered them faster, and backed them with technology that European consumers actually want. That’s how markets are supposed to work. Europe still has real strengths — premium engineering, design excellence, regulatory credibility — and those strengths give it a genuine path to compete. However, that path requires urgency, investment, and a willingness to make structural decisions that legacy interests have resisted for years. The window to respond is open. It won’t stay that way forever.